Consumer Spec - Pre Market Wrap

WEN (-) JPM Underweight, DPZ (-) Redburn Sell, ONON (-) Jefferies Cautious | Crude Rip Pressures CCL/RCL/NCLH, QSR Value War Intensifies, WHR PT Cut, RH OW Reiterate, WMT 1FQ27 Preview, Hormuz Closed

US futures are slightly lower (SPX -5bps, NDX -10bps, RTY -5bps) while WTI jumped 2.2% to $97.60 and UST 10yr yields rose 3bps to 4.385% as US/Iran peace talks stalled, with Trump calling Tehran's reply "totally unacceptable."

Key events this week include the Trump/Xi meeting in China (Thu/Fri), Bessent's Japan/South Korea visit, and major US data releases (CPI Tue, PPI Wed, Retail Sales Thu).

HIGH SIGNAL REPORTS TODAY:

(-) WEN: JPM Underweight + BMO negative note

(-) DPZ: I think this Redburn note will have impact today

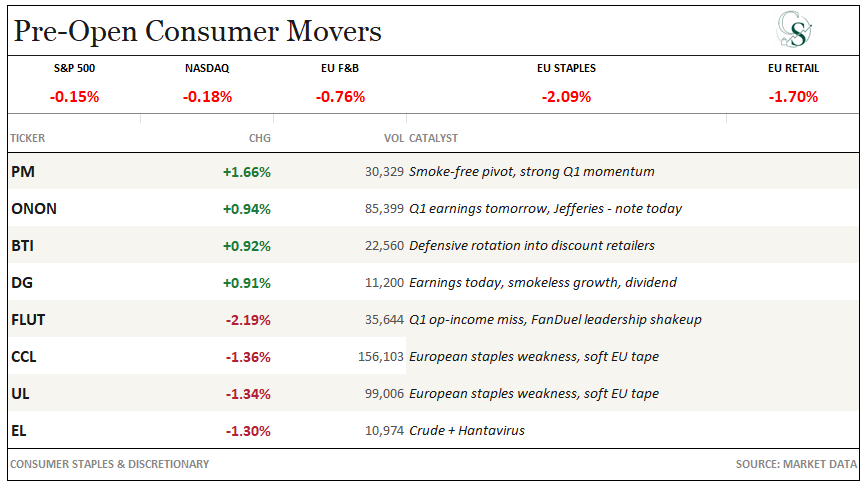

(-) ONON: Jefferies negative on channel checks although they reiterate prior reports

(-) CCL/RCL/NCLH: Not a report but group may trade weak on Hantavirus news+ crude +

CONSUMER PRE-MARKET:

Pre-market tone is very quiet but risk-off in Europe as crude rips again on geopolitics. Brent +2.7% to ~$104 with Hormuz still effectively shut keeps the pressure on cruise bunker (CCL, RCL, NCLH), airline-adjacent leisure (MAR, HLT, MTN), and QSR commodity baskets where chicken/beef are already squeezing WEN, MCD, YUM, TXRH. Sell-side is leaning harder into the restaurant bear case this morning: JPM moves WEN to Underweight calling it the #6 brand from #4 twenty years ago, BMO trims alongside, and Rothschild Redburn cuts DPZ to Sell flagging structurally lower pizza share of the delivery pool. WHR also takes a PT cut at Citi. Watch breadth in restaurants and big-ticket discretionary.

Earnings

No covered-name earnings prints this morning.

Analyst Actions

WEN: JPMORGAN DOWNGRADES TO UNDERWEIGHT $6 PT, BMO TRIMS TO $8 — BEAR CASE HARDENS

JPMorgan’s Rahul Krotthapalli moved Wendy’s from Neutral to Underweight with a Dec-26 PT of $6 (from $7), citing four pillars: continued declines in headline US SSS with limited visibility into the guided 2H26 inflection, lack of permanent leadership and ongoing sub-optimal capital allocation, “too little, too late” value repositioning against an intensifying MCD value push and BK’s resurgence, and high net leverage limiting reinvestment flexibility through F28. Krotthapalli flags WEN has slipped to the #6 US restaurant brand by sales dollars from #5 ten years ago and #4 twenty years ago. Separately, BMO’s Andrew Strelzik lowered his PT to $8 (from $9) while maintaining Market Perform. Bull case rests on franchisee health and eventual leadership reset; bear case is a structurally challenged value proposition into a price-war intensification.

DPZ: ROTHSCHILD REDBURN CUTS TO $290 PT SELL CITES STRUCTURAL DELIVERY SHARE LOSS

Rothschild Redburn analyst Chris Luyckx lowered Domino’s PT to $290 (from $340) maintaining a Sell rating, implying ~11% downside. The thesis: the US Restaurant Delivery market has expanded at an unprecedented pace, but the growth has accrued almost entirely to non-pizza operators via third-party aggregators, with pizza’s share of the pool now halved. Luyckx argues Domino’s first-party delivery business has been running flat-to-negative beneath a headline comp increasingly reliant on third-party volume that masks underlying weakness. While the closure of ~450 competitor stores has been cited by the company as an offset, on Redburn’s bottom-up analysis only half the EPS uplift consensus models actually flows through. New PT is $290 vs. prior $340. The note is one of the more structurally bearish framings on DPZ in recent months and challenges the bull case that the franchisee health and unit economics story can offset category share erosion to aggregator-delivered non-pizza occasions.

WHR: CITI LOWERS PT TO $50 FROM $60 MAINTAINS NEUTRAL ON APPLIANCE PRESSURE

Citi analyst Kyle Menges lowered the price target on Whirlpool to $50 (from $60) while maintaining a Neutral rating. No specific commentary was provided in the note, but the move comes amid an ongoing soft backdrop for big-ticket appliances tied to a sluggish existing home sales market, persistent input cost pressure, and continued Asian import competition. Bull case for WHR rests on Section 232 tariff enforcement helping domestic price realization and an eventual housing turn; bear case is sustained R&R weakness, continued promotional pressure at retail, and limited operating leverage. The Neutral rating signals Citi sees the risk/reward as still balanced rather than constructive at current levels.

RH: REITERATE OW, $240 PT, MULTIPLE TAILWINDS CONVERGING

Morgan Stanley keeps an OW and $240 PT on RH, framing the name as high-beta but with risk/reward skewed asymmetrically to the upside as several historic overhangs simultaneously fade. The firm flags the May launch of the Estates collection (price points ~20% above current, accretive to sales/GM), peaking European expansion drag, easing tariff pressure that could flip positive, inventory normalization, and a notable philosophical pivot toward balance sheet repair, with mgmt targeting debt-free in three years against ~$2.4bn (~$150/share) of net financial debt. The analyst notes RH owns 13 properties (~$140m invested in Aspen alone) where monetization at ~5% prime retail cap rates vs ~6.4% WACD enables deleveraging plus P&L arbitrage, and adds the stock trades at ~6.7x ‘27e MS-adj EV/EBITDA on a normalized ~20% margin, a ~30% discount to the ~9x long-term average. PT is built on 11.5x ‘27e MS-adj EBITDA of $639m.

ONON: 1Q PREVIEW, RISKS BUILDING, PT $24

Jefferies stays cautious into ONON’s 1Q with a $24 PT (10x F’27e EBITDA), arguing the brand is “working harder for less” as paid search reached 77% of on.com traffic in March (~3x peers), bounce rate climbed to 54% (vs ~40% peer avg), and core SKUs are surfacing at outlets and Nordstrom Rack at up to 50% off. The firm models 1Q revs of CHF 817M (vs SA CHF 821M) with GM tracking 60.3% against mgmt’s 63%+ FY guide, citing channel mix and tariff pressure, and sees any beat coming from APAC while US decelerates and wholesale cracks. The analyst notes Americas growth has decayed from +83% in ‘22 to +18% in ‘25 with their model pointing sub-10% in ‘26 and barely positive in ‘27, while Nike reclaims shelf and drives 20%+ running category growth. The analyst adds ONON’s 15x FY2 EBITDA vs 8x peer avg leaves no room for error, with the co-CEO transition and FY guide of >23% CC growth and 18.5-19.0% EBITDA margins as key watch items; risk/reward skewed firmly to the downside.

WMT: MORGAN STANLEY REITERATE OW, $140 PT, MODEST UPSIDE INTO 1FQ27

Morgan Stanley reiterates OW and $140 PT on WMT into the May 21 print, expecting modest upside to 1FQ27e with F’27 guidance unchanged for now given the recent gas price spike. The firm sees U.S. comp landing above the 3.9% consensus and in line with buyside expectations of +4.0% to +4.5%, despite a ~100bps pharmacy drag from Maximum Fair Pricing and lower-priced GLP-1 mix, supported by trade-down, food inflation (+2.3% Feb/Mar), and an AlphaWise survey pointing to record Walmart+ membership. The analyst notes ~2pts of upside to consensus’s +8% adj OI/EPS growth, with FX (MXN +16% vs USD) contributing ~1%/~2% to sales/OI, eCommerce momentum sustaining (4FQ26: +27% U.S. eComm, +41% Walmart Connect), and diesel/freight a ~$100m 1Q hit but ~$1bn annualized headwind pre-mitigation. The analyst adds intra-quarter mgmt meetings flagged a healthy 3P marketplace and early export of the U.S. Advertising/Marketplace model internationally; 2FQ27e outlook likely calls for +3.5-4.5% net sales (cc) and +8-10% adj OI growth as the ~$450m 2FQ26 GL claims headwind anniversaries.

Macro & News

QSR: PEER READ-THROUGH FROM JPM WENDYS DOWNGRADE FLAGS INTENSIFYING VALUE WAR

Within JPMorgan’s WEN downgrade, the analyst explicitly cites MCD’s “intensifying value efforts” alongside BK’s resurgence as a key competitive pressure point eroding Wendy’s share of the QSR value occasion. The read-through for MCD is mixed: on the constructive side, JPM’s framing positions MCD as a share gainer in the current value cycle and reinforces the narrative that MCD’s value platform is working at the franchisee P&L level. On the cautious side, escalating QSR value warfare typically compresses category-wide check and franchisee margins, and history suggests these cycles end with structurally lower industry profitability before pricing power returns. For MCD specifically, the question into Q2 is whether US comps can stay positive against a rapidly weakening peer set (WEN -SSS, traffic broadly soft) without resorting to deeper national-deal investment.

CRUDE: BRENT +2.7% TO 104 STRAIT OF HORMUZ STAYS CLOSED PRESSURE ON LEISURE QSR

Oil rallied sharply Monday after President Trump called Iran’s response to the US peace proposal “unacceptable,” with the Strait of Hormuz still largely closed and supply fears reasserting themselves. Brent climbed $2.70 or 2.67% to $103.99 a barrel at 0902 GMT; WTI was at $97.66, up $2.24 or 2.35%, with both contracts hitting $105.99 and $100.37 respectively earlier in the session. Last week both contracts recorded 6% losses on ceasefire hopes. PVM’s John Evans said the US and Iran are “as far away from agreement as when this supposed ceasefire started” and sees nothing changing before Trump visits Beijing Wednesday. Saudi Aramco’s Amin Nasser said the world has lost ~1 billion barrels over the past two months and markets will take time to stabilize even if flows resume. Read-through is negative for cruise bunker spend (CCL, RCL, NCLH), travel demand elasticity (MAR, HLT, MTN, VAC), QSR/restaurant commodity baskets, and discretionary wallet share as gasoline pump prices reset higher into summer driving season.